TDS on Salary in India. Complete Guide (Section 192)

What is TDS and Why it is Deducted on Salary ?

The total income earned by a person (Assessee) in a financial year, known as the previous year (P.Y.), is taxed in the following assessment year (A.Y.).

For example, income earned during P.Y. 2024–25 is taxed in A.Y. 2025–26.

However, income tax is often collected during the previous year itself through the following methods:

- Tax Deducted at Source (TDS)

- Tax Collected at Source (TCS)

- Advance Tax Payments

The purpose of these early tax deductions is to ensure that taxpayers don’t feel the burden of paying taxes all at once. These tax amounts (TDS, TCS, etc.) are adjusted against the total tax payable by the assessee. When filing the income tax return, if there’s any balance tax payable after adjusting all deductions and exempt allowances. If excess TDS is deducted by employer then it can be refunded by filing Income Tax Returns on time.

This section casts an obligation on every person responsible for paying any income chargeable to tax under the head ‘Salaries’ to deduct income-tax at the time of payment on the amount payable.

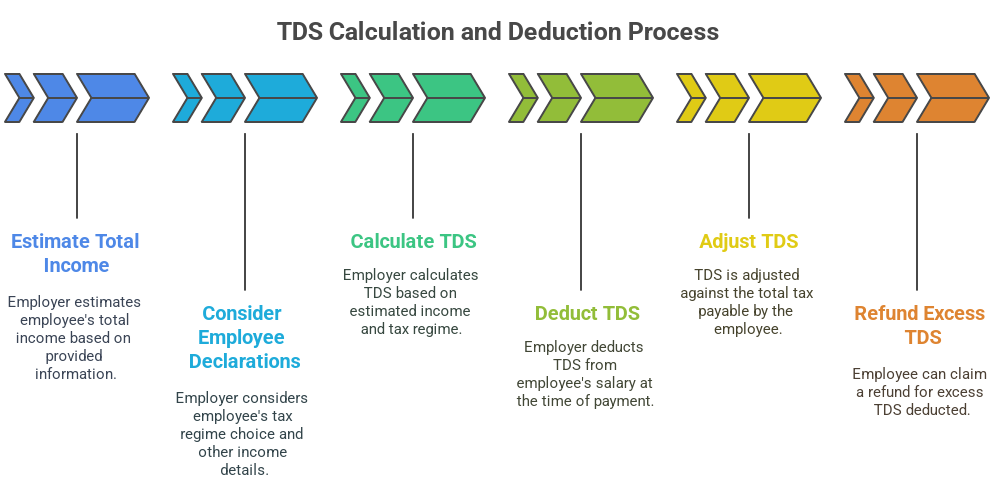

How TDS is calculated On salary ? What points are consider for deduction of TDS on salary ?

- In First step employer estimate the expected Total Income based on the information provided by the employee. Total income includes Income from Salary, Income from house property, and Other sources.

- A taxpayer with salary income and other taxable income can provide their employer with details of:

(a) Other income and any tax deducted under other provisions,

(b) Any loss under the head ‘Income from house property’ if the taxpayer intends to opt out of the default tax regime under Section 115BAC(1A).

The employer must consider these details when calculating TDS. - If an assessee works for more than one employer in a financial year either simultaneously or after switching jobs they can provide details of salary received, tax deducted, and other relevant information from the previous employer to the current one. The current employer should then consider this information and deduct TDS on the total income from both employers for the year.

- Employers must ask employees to declare their chosen tax regime each year. Based on this, TDS will be calculated under Section 192. If no declaration is made, it will be assumed that the employee is under the default new tax regime (Section 115BAC). Note: This declaration is only for TDS and not a formal option under Section 115BAC(6), which must be exercised separately.

- If an employee chooses to opt out of the default New tax regime under Section 115BAC, the employer must calculate TDS based on the average tax rate applicable for that financial year, using the employee’s estimated total income. From AY 2024-25 or FY 2023-24 if the employee does not provide any information, TDS will be deducted based on the New income tax slab rates under the default tax regime. Note: TDS on salary is deducted only at the time of payment.

- Average rate of income-tax means the rate arrived at by dividing the amount of income tax calculated on the total income, by such total income.

- Under Sections 192(1A) and (1B), an employer can choose to pay tax on non-monetary perquisites instead of deducting it from the employee’s salary. This tax is calculated at the average rate based on the employee’s total salary and must be paid monthly along with TDS on regular salary and allowances.

- For salary payments to employees of the government, companies, co-operative societies, local authorities, and similar bodies, TDS should be deducted after allowing relief under Section 89, if applicable.

- To ease cash flow issues for employees, Section 192(1B) has been extended to include any tax deducted or collected at source for TDS purposes. Starting from 1.10.2024, employees can inform their employers about:

(a) Other taxable income (excluding losses),

(b) Tax deducted or collected under any other provision,

(c) Any loss under “Income from house property” if opting out of the default tax regime under Section 115BAC(1A).

The employer must consider these details when calculating TDS. However, TDS on salaries should only be reduced for house property losses (up to ₹2,00,000) and taxes already deducted or collected. - Employers paying salary must collect proof or details of tax-saving claims (like deductions or loss set-off) from employees in the prescribed format. This helps in estimating income and calculating TDS under Section 192.

- If an employee chooses to opt out of the default tax regime under Section 115BAC(1A), they must submit Form 12BB with supporting documents as required by Rule 26C, so the employer can compute the correct TDS.

TDS deduction example

Understanding how TDS (Tax Deducted at Source) is calculated on salary can help employees estimate their monthly deductions more accurately. Here’s a simple example to explain the process:

| PARTICULARS | AMOUNT (₹) |

| Monthly Salary | ₹ 1,00,000 |

| Annual Salary | ₹ 12,00,000 |

| Tax on Total Salary (as per slabs) | ₹ 1,42,500 |

| Add: Education & Health Cess @ 4% | ₹ 5,700 |

| Total Tax Payable | ₹ 1,48,200 |

| Average TDS Rate | (₹ 1,48,200 / ₹12,00,000) × 100 = 12.35% |

| Monthly TDS Deduction | 12.35% of ₹ 1,00,000 = ₹ 12,350 |