Key Terms in the Income Tax Act Explained

Para : To understand the rules in the Income Tax Act, it’s important to clearly know the meanings of some important terms like ‘assessment year’, ‘person’, ‘assessee’, ‘income’, and so on. To find out what these terms mean, we first need to see if they are defined in the Act.

1) Assessee [Section 2(7)]

“Assessee” refers to any person who has to pay tax or any other amount under the Income Tax Act. It also includes:

- Anyone for whom the tax department starts a case to check:

- their own income

- someone else’s income for which they are responsible,

- a loss they or someone else had, or

- a refund that they or someone else should get

- Anyone who is considered an assessee by any rule in the Act.

- Anyone who is treated as an “assessee-in-default” under the Act (meaning they didn’t do something they were supposed to, like deduct or pay tax).

Every assessee is a “person,” but not every “person” is necessarily an assessee.

2) Assessment [Section 2(8)]

This is the process used by the Income Tax Department to calculate how much income a person (assessee) has earned. An officer from the department (Assessing Officer) does this. The income can be assessed for the first time or rechecked if it was already assessed earlier.

There are different types of income tax assessments:

- Self-assessment (Section 140A) – The taxpayer calculates and pays their own tax.

- Summary assessment (Section 143(1)) – A quick check of the return using computer processing, without calling the taxpayer.

- Scrutiny assessment (Section 143(3)) – A detailed check where the officer may ask for documents and explanations.

- Best judgment assessment (Section 144) – If the taxpayer doesn’t file a return or cooperate, the officer makes an estimate based on available information.

- Re-assessment or income escaping assessment (Section 147) – If the officer finds that some income was not assessed earlier, they can reopen the case and reassess it.

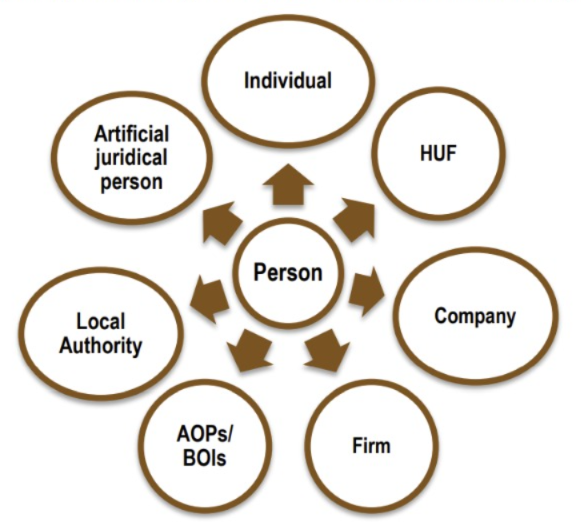

3) Person [Section 2(31)]

To understand who an “assessee” is, we also need to understand what the word “person” means, because the two are closely related. The term “person” is very important because income tax is charged on every “person.”

The definition of “person” in the Income Tax Act is inclusive, meaning it gives examples but not a complete list. The Act recognizes different types of “persons,” which are shown in the diagram below.

We may briefly consider some of the above seven categories of assessees each of which constitute a separate unit of assessment or a separate tax entity.

(i) Individual

The term ‘individual’ refers to a natural person, meaning a human being. This includes both males and females, as well as minors and persons of unsound mind. However, in cases where the individual is a minor or mentally unfit, the income tax assessment may be done under section 161(1) on their guardian or manager who is entitled to receive their income. If the person has passed away, the assessment is carried out on their legal representative.

(ii) HUF

Under the Income-tax Act, 1961, a Hindu Undivided Family (HUF) is considered a separate legal entity for tax purposes. It is included in the definition of a “person” under section 2(31), and since income tax is charged on every person, a HUF is also required to pay tax. Although the Income-tax Act does not define the term “Hindu Undivided Family,” it is defined under Hindu Law as a family made up of male members descended from a common ancestor, along with their wives and daughters.

(iii) Company [Section 2(17)]

For income tax purposes, the term ‘Company’ has a broader meaning than what is given in the Companies Act, 2013. According to the Income-tax Act, a ‘Company’ includes:

(a) Any Indian company as defined in the law,

(b) Any company or organization formed under the laws of another country (foreign company),

(c) Any group or body that was taxed as a company under the old Income-tax Act of 1922 or for assessment years before April 1, 1970,

(d) Any group or organization—Indian or foreign, registered or not—that the Central Board of Direct Taxes (CBDT) declares to be treated as a company for certain assessment years.

(iv) Firm [Section 2(23)]

The terms ‘firm’, ‘partner’, and ‘partnership’ mean the same as they do in the Indian Partnership Act, 1932. These terms also include limited liability partnerships (LLPs) and their partners, as defined in the LLP Act, 2008. An LLP combines features of both a company and a traditional partnership, since the partners’ liability is limited to the amount they agreed to contribute. Also, for income tax purposes, even a minor who is admitted to enjoy the benefits of an existing partnership is treated as a partner.

(v) Association of Persons (AOP)

When people come together to run a business or project jointly but are not legally considered a partnership, they are taxed as an Association of Persons (AOP). To be considered an AOP, the individuals must come together with a common goal or activity, and the aim should be to earn income. Just receiving income together is not enough. For example, co-heirs, co-legatees, or co-donees who join efforts for a shared purpose will also be taxed as an AOP.

(vi) Body of Individuals (BOI)

A Body of Individuals (BOI) refers to a group of people who come together to carry out an activity, either for income or not. It includes people like executors or trustees, who receive income together and are taxed in the same way as the individuals they represent. For example, co-executors or co-trustees are treated as a BOI because their rights and interests cannot be separated. If a BOI has already paid tax on the income, the individuals receiving a share of that income do not need to pay tax again. Examples of BOIs include mutual trade associations or members’ clubs.

Section 2(31) explains that an Association of Persons (AOP), BOI, local authority, or any artificial legal entity (like a company or trust) is considered a “person” under the Act, even if their purpose is not to earn income or profit. This means that even if these entities aren’t formed to make money, they are still covered by the Income Tax Act.

Difference between AOP and BOI:

- In a BOI, only individuals can be members, while in an AOP, any entity (like a company or firm) can be a member.

- In an AOP, members come together willingly with a common goal or purpose, but in a BOI, this common intention may not always be present.

(vii) Local Authority

The term local authority refers to entities like a municipal committee, district board, port commissioners, or any other authority that the government has given the responsibility to manage or control a municipal or local fund.

Note: A local authority is only taxed on the income it earns from any business it operates, but this only applies if the income is not from providing goods or services within its own area. However, income from supplying water or electricity, even outside the local authority’s area, is exempt from tax.

(viii) Artificial Juridical Persons

Artificial Juridical Persons are entities that are not natural people but are still considered separate legal entities by the law. This category includes any artificial persons that don’t fit into other categories of persons. Examples of Artificial Juridical Persons include deities, Bar Councils, and Universities.

4) Income [Section 2(24)]

The definition of income under the Income-tax Act, 1961 starts with the words “Income includes,” which means it’s an inclusive definition, not exhaustive. This allows the definition to cover not only the items specifically mentioned but also any other types of income that may come up.

Section 2(24) of the Act lists what is considered income. Some examples include:

- Profits and gains from any business or profession.

- Dividends received.

- Voluntary contributions received by certain charitable or religious trusts or institutions.

- Value of perquisites or profits in lieu of salary (like benefits or allowances) that are taxable.

- Special allowances granted to meet the expenses of office duties.

- Allowances for personal expenses at work or where the person lives.

- Benefits or perquisites from a company (for directors or people with a significant interest in the company, and their relatives).

- Deemed profits (profits assumed to be income under certain sections of the Act).

- Capital gains that are taxable.

- Profits from insurance business by mutual insurance companies or cooperative societies.

- Banking profits by cooperative societies that provide credit facilities.

- Winnings from lotteries, gambling, betting, or games of any kind, including TV game shows or puzzles.

- Any contributions made by employees to a Provident Fund (PF), Superannuation Fund, Employees State Insurance (ESI), or other welfare funds are considered income.

- Any amount received under a Keyman insurance policy (a life insurance policy taken by a business on the life of an important employee or someone connected to the business) is treated as income. This includes any bonuses paid on such a policy.

- Any sum received under an agreement where a person agrees not to engage in business activities, share certain knowledge or intellectual property (like patents, trademarks, etc.), is considered income.

- The fair market value of inventory that is converted into or treated as a capital asset is considered income.

- Any advance payment received for the transfer of a capital asset, which is forfeited when the deal doesn’t go through, is treated as income.

- Any sum of money or property received without consideration, or for less than its actual value, is considered income.

- Any compensation or payment received due to the termination or change of employment conditions is considered income.

- Any specified sum received by a unit holder from a business trust in relation to a unit held during the previous year is treated as income.

- Bonus or sum received under a life insurance policy (other than a ULIP or Keyman policy) that exceeds the premiums paid during the policy term is considered income.

- Any subsidy, grant, cash incentive, duty drawback, waiver, concession, or reimbursement from the government, or any authority or agency, is included as income.

4) Maximum marginal rate and Average Rate of tax

According to Section 2(10), the “Average Rate of Tax” is calculated by dividing the total income tax by the total income. This gives the average rate at which the income is taxed.

As per Section 2(29C), the “Maximum Marginal Rate” refers to the highest rate of income tax (including any surcharge) that applies to the highest income bracket for an individual, Association of Persons (AOP), or Body of Individuals (BOI). This rate is specified in the Finance Act for the relevant year.

5) Assessment year [Section 2(9)]

The term “Assessment Year” is defined under Section 2(9). It refers to a 12-month period starting on 1st April each year. The previous year is the year in which income is earned, and that income is taxed in the assessment year, which follows right after the previous year.

For example, income earned in the previous year (2024-25) will be taxed in the assessment year (2025-26). The assessment year always starts on 1st April and lasts for 12 months.

6) Previous year [Section 3]

The “Previous Year” refers to the financial year immediately before the assessment year. As mentioned earlier, the income earned during the previous year is taxed in the assessment year.

If a new business or profession is started during the financial year, then the previous year will start from the date the business is set up and end on 31st March of that same financial year.

Similarly, if a new source of income is created during the financial year, the previous year will begin from the date the source starts and end on 31st March of the same year.